Buy Now, Pay Later (BNPL) is a point-of-sale financing option that has grown increasingly popular in recent years, especially among younger generations.

BNPL solutions emerged in the early 2010s to address pain points around financing – mainly, the complexity and high fees and APRs associated with credit cards. As shown in a study by Insider Intelligence, these often excessive fees have led consumers to seek alternative payment methods, directly contributing to BNPL’s success.

As an alternative to credit cards and other financing forms, BNPL solutions allow shoppers to purchase products and pay in predetermined installments over time. These solutions often have little to no interest rates and hidden fees, meaning no additional cost to the customer.

The size of the U.S. BNPL lending market was worth around a few billion U.S. dollars in 2019 but is estimated to grow by 1,200 percent by 2024.

With BNPL’s rapidly growing implementation, retailers looking to gain a market edge are presented with a real opportunity – they just need to seize it.

💬 You might also be interested in:

Shopify SEO vs WordPress SEO: Who Win 2024?

Shopify Vs Square: Which One Suits Your Business Best In 2024?

Buy Now, Pay Later’s Target Audience – Who Are They?

The target customer for Buy Now, Pay Later (BNPL) services leans heavily towards younger generations:

- Millennials: This demographic, born between 1981 and 1996, has shown a significant increase in BNPL adoption, with usage rates more than tripling since 2019.

- Gen Z: Even more impressive is the growth of BNPL among Gen Z (born between 1997 and 2012). Studies by Forbes report a staggering 600% increase in BNPL usage within this age group since 2019.

There are several reasons why these younger generations are drawn to BNPL!

- Tech-Savvy and Convenience-Driven: Millennials and Gen Z are comfortable with digital transactions and appreciate the ease and speed of BNPL checkout processes.

- Budget-Conscious: These age groups may not have established credit or may be wary of traditional credit cards with high-interest rates. BNPL offers a way to manage purchases without accruing significant debt as long as payments are made on time.

- Desire for Instant Gratification: The ability to acquire desired items immediately and spread out payments aligns well with the spending habits of younger generations.

While adoption among older generations (Gen X and Baby Boomers) is on the rise, the current trend suggests that BNPL may become the preferred payment method for Millennials and Gen Z in the future.

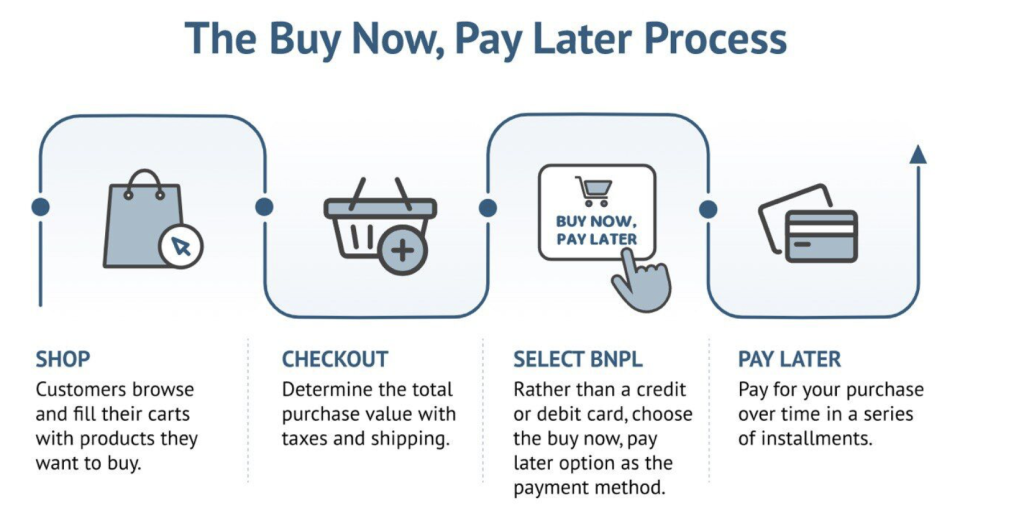

How Buy Now, Pay Later Works for Consumers and Merchants

Buy Now, Pay Later (BNPL) has emerged as a popular alternative payment method, particularly among younger generations. Here’s a breakdown of how it functions for both consumers and merchants!

For Consumers

During online checkout, BNPL providers like Klarna or Afterpay offer the option to receive the product immediately while deferring payment.

Typically, you can choose between three or four interest-free installments spread over a specific timeframe. Alternatively, some BNPL services offer a “Pay Later” option where the full amount is due within 30 days, again without interest charges.

It provided you fulfill your payment obligations on time. There are no additional fees or interest accrued on your purchases.

The Checkout Experience

- Find your desired item and add it to your cart.

- Proceed to checkout.

- Alongside traditional payment methods (credit/debit cards, PayPal), you’ll see BNPL options (e.g., Pay with Klarna, Pay with Afterpay).

- Choose your preferred BNPL payment plan (Pay Later in 30 days, split into installments, or potentially finance larger purchases with extended payment terms that might incur interest).

- Complete the checkout process.

Additional Options

- Physical/Virtual BNPL Cards: BNPL providers offer physical or virtual cards in some regions. This allows you to use BNPL at stores that don’t typically offer it. Purchases are linked to your BNPL account, and you can choose to pay later (within 30 days) or finance the cost over time (potentially with interest).

- In-Store BNPL: Some brick-and-mortar stores are integrating BNPL options. You can often generate a QR code within your BNPL app, which the cashier scans at checkout to complete the purchase. You then manage your payment schedule through the BNPL app.

Benefits for Consumers!

- BNPL allows you to spread out the cost of purchases, potentially enabling you to afford items you might not be able to with a single upfront payment.

- You can control your payment schedule by choosing the repayment option that best suits your budget.

- As long as you make your payments on time, you won’t incur any additional interest fees.

For Merchants

- Enhanced Conversion Rates: By offering BNPL options, merchants can potentially increase their conversion rates by making purchases more accessible to budget-conscious consumers.

- Reaching New Customers: BNPL can attract new customers who may not have access to traditional credit cards or prefer alternative payment methods.

- Faster Checkout Process: BNPL streamlines the checkout experience, potentially leading to fewer abandoned carts.

- Fees for Merchants: Merchants typically pay BNPL providers a commission (2-6%) and a fixed fee for each BNPL transaction.

Why Buy Now, Pay Later Holds Allure for Consumers?

The rising popularity of Buy Now, Pay Later (BNPL) can be attributed to several factors that resonate with consumers!

Following the COVID-19 pandemic, consumers have grown wary of high credit card interest rates, declining credit limits, and underwhelming rewards programs. This has opened the door for alternative payment methods like BNPL.

Plus, Unlike credit cards that profit from interest and late fees, BNPL services generally offer lower fees and interest rates, or even no interest at all if payments are made on time. This makes BNPL a potentially more budget-friendly financing option for purchases.

Moreover, for consumers who prefer not to use credit cards or carry cash, BNPL presents a convenient and flexible payment alternative. Approvals are often instantaneous at checkout, making it a seamless in-store experience.

For online purchases, BNPL allows you to secure your desired items upfront with the flexibility to spread out payments, ensuring on-time delivery without the worry of forgetting upcoming payments.

In simpler terms, BNPL offers consumers

- A perceived escape from the high costs associated with traditional credit cards.

- A way to manage their budget more effectively by spreading out payments.

- A convenient and user-friendly payment experience.

These factors have contributed significantly to the growing adoption of BNPL services, particularly among younger generations.

How Buy Now, Pay Later Benefits Retailers?

Buy Now, Pay Later (BNPL) isn’t just popular with consumers; it offers significant advantages for retailers as well.

Let’s delve into how BNPL benefits businesses!

Guaranteed Upfront Payment

Even though customers spread out their payments, retailers receive the full purchase amount immediately from the BNPL provider (like Klarna or Affirm) upon checkout. This eliminates the risk of customer defaults for the retailer.

Smart Risk Management

BNPL companies leverage advanced algorithms to assess both customer and retailer creditworthiness. This mitigates risk for both parties, ensuring a secure transaction.

Attracting New Customers

The “try before you buy” mentality can be a hurdle for online retailers. BNPL services, often coupled with features like free returns and dedicated customer support, allow customers to overcome this barrier.

This flexibility encourages exploration and purchase decisions, potentially attracting new customers who might otherwise hesitate.

Enhanced Customer Experience

Offering BNPL caters to the desire for a smooth and positive shopping experience, particularly among younger generations (Millennials and Gen Z). This includes features like free returns and a user-friendly platform that streamlines the buying process.

Increased Sales Conversions

The sticker shock of a large purchase price or the fear of high credit card interest rates can deter customers. BNPL options alleviate this concern by breaking down the cost into manageable installments.

Studies by the Baymard Institute highlight price as a major reason for cart abandonment. BNPL can significantly reduce this by making expensive items more accessible.

Higher Customer Lifetime Value (LTV)

By offering BNPL, retailers can attract new customers, particularly younger demographics. The positive shopping experience, coupled with the flexibility of BNPL, encourages repeat business and potentially larger purchases (larger average basket sizes).

Since customer satisfaction is crucial for retention, these positive experiences translate into loyal customers who return for future purchases.

In essence, BNPL creates a win-win scenario for both consumers and retailers. Consumers gain flexibility and control over their purchases, while retailers benefit from increased sales, a wider customer base, and potentially higher customer lifetime value.

How Do You Choose The Right Buy Now, Pay Later Provider For Your Business?

Integrating Buy Now, Pay Later (BNPL) into your business strategy can be wise. However, selecting the most suitable BNPL provider requires careful consideration. Here are some key factors to evaluate:

1. Understanding Your Business and Customers

- Product Range: Consider the types of items you sell. BNPL providers offering longer repayment terms (several months to years) might be ideal for high-value products. Conversely, lower-priced items might better suit shorter repayment plans with fewer installments.

- Target Audience: Identify your ideal customer. Understanding their demographics, spending habits, and preferred payment methods will guide your selection.

2. Analyzing BNPL Provider Options

- Repayment Terms: Each BNPL provider offers various installment plans and durations. Evaluate your average order value (AOV) to determine if shorter or longer repayment terms best suit your business model.

- Credit Limits: BNPL providers typically have minimum and maximum purchase amounts their customers can finance. Ensure the provider’s credit limits align with your AOV and your business’s creditworthiness.

- Geographic Coverage: Consider the markets you operate in or plan to expand into. Some BNPL providers have regional limitations. You might need to consider using multiple providers depending on your target markets and budget.

Additional Considerations

- Integration Fees and Transaction Costs: Compare the fees associated with integrating the BNPL service with your existing platform and the transaction costs charged by each provider.

- Approval Rates: Investigate the typical customer approval rates for each BNPL provider. Higher approval rates can lead to a smoother customer experience and potentially fewer abandoned carts.

- Customer Support: Assess the quality of customer support offered by each BNPL provider. This ensures a seamless experience for both you and your customers in case of any issues.

- Reputation and Brand Recognition: Consider the reputation and brand recognition of each BNPL provider. Partnering with a well-established and trusted provider can enhance customer confidence in your business.

By carefully evaluating these factors, you can select a BNPL provider that aligns with your business goals, target audience, and operational needs. This will allow you to leverage the benefits of BNPL to attract new customers, increase sales conversions, and potentially boost customer lifetime value.

The Concluding Perspective

As younger generations begin to establish themselves and gain greater purchasing power – and as credit cards continue declining in popularity – expect the desire for flexible payment options to increase.

Buy Now, Pay Later presents an alternative, flexible option to disrupt the payments industry, draw customers away from credit card companies, and enable them to spread purchase payments over time – without the burden of accruing uncomfortable interest fees.

Digital financing options will only continue growing alongside an increasingly technological world. For organizations wanting to remain at the forefront – and cater to a changing customer base – implementing Buy Now, Pay Later into a storefront can only serve to benefit them.

Adopting flexible payment solutions allows businesses to meet evolving consumer needs and preferences. As financial stresses persist, providing accessible financing tools will be key to capturing market share.

Buy Now, Pay Later (BNPL) in E-commerce: Frequently Asked Questions

1. What is The Origins of BNPL?

The concept of BNPL, or deferred payments, has been around for a long time, offering an alternative to upfront purchases.

However, the current iteration of BNPL with digital payment solutions emerged in the early 2010s. Pioneering companies like Affirm and Klarna (Europe) and Afterpay (Australia) played a key role in its development.

2. Should You Offer BNPL on Your Website?

The answer is a strong yes, if possible. With BNPL’s surging popularity, businesses that don’t offer it risk falling behind competitors. BNPL offers advantages for both you and your customers by providing greater flexibility in the buying process.